All courses

Agentic AI

Agentic AI

IIIT Bangalore

Executive Programme in Generative AI for LeadersArtificial Intelligence

Degree / Exec. PG

IIIT Bangalore

Executive Diploma in Machine Learning and AI

OPJ Global University

Master’s Degree in Artificial Intelligence and Data Science

Liverpool John Moores University

Master of Science in Machine Learning & AI

Golden Gate University

DBA in Emerging Technologies with Concentration in Generative AIExecutive Certificate

IIITB & IIM, Udaipur

Chief Technology Officer & AI Leadership ProgrammeIIIT Bangalore

Executive Programme in Generative AI for Leaders

upGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftupGrad | Microsoft

Gen AI Mastery Certificate for Data AnalysisupGrad | Microsoft

Gen AI Mastery Certificate for Software DevelopmentupGrad | Microsoft

Gen AI Mastery Certificate for Managerial ExcellenceOffline Bootcamps

upGrad

Data Science and AI-MLDoctorate

For All Domains

IIITB & IIM, Udaipur

Chief Technology Officer & AI Leadership Programme

Swiss School of Business and Management

Global Doctor of Business Administration from SSBM

Edgewood University

Doctorate in Business Administration by Edgewood UniversityGolden Gate University

Doctor of Business Administration From Golden Gate University

Rushford Business School

Doctor of Business Administration from Rushford Business School, SwitzerlandGolden Gate University

Master + Doctor of Business Administration (MBA+DBA)-d9bdeff6165f4eb1ba2adcebde78e961.svg)

University of Waterloo

Chief Technology and AI Officer ProgramLeadership / AI

Golden Gate University

DBA in Emerging Technologies with Concentration in Generative AIMachine Learning

Machine Learning

Data Science

Degree / Exec. PG

O.P Jindal Global University

Master’s Degree in Artificial Intelligence and Data ScienceIIIT Bangalore

Executive Diploma in Data Science & AILiverpool John Moores University

Master of Science in Data ScienceExecutive Certificate

upGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftupGrad | Microsoft

Gen AI Mastery Certificate for Data AnalysisupGrad | Microsoft

Gen AI Mastery Certificate for Software DevelopmentupGrad | Microsoft

Gen AI Mastery Certificate for Managerial ExcellenceupGrad | Microsoft

Gen AI Mastery Certificate for Content CreationOffline Bootcamps

upGrad

Data Science and AI-MLupGrad

Data AnalyticsMBA

Masters

Paris School of Business

Master of Science in Business Management and TechnologyO.P.Jindal Global University

MBA (with Career Acceleration Program by upGrad)Edgewood University

MBA from Edgewood UniversityO.P.Jindal Global University

MBA from O.P.Jindal Global UniversityGolden Gate University

Master + Doctor of Business Administration (MBA+DBA)Executive Certificate

IMT, Ghaziabad

Advanced General Management ProgramMarketing

Executive Certificate

Offline Bootcamps

upGrad

Digital MarketingManagement

Degree

O.P Jindal Global University

MSc in International Accounting & Finance (ACCA integrated)Paris School of Business

Master of Science in Business Management and Technology

Golden Gate University

Master of Arts in Industrial-Organizational PsychologyExecutive Certificate

IIIT-B & IIM, Udaipur

Chief Technology Officer & AI Leadership Programme

IIM Kozhikode

Human Resource Analytics Course from IIM-KupGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftEducation

Education

Northeastern University

Master of Education (M.Ed.) from Northeastern UniversityEdgewood University

Doctor of Education (Ed.D.)Edgewood University

Master of Education (M.Ed.) from Edgewood UniversityCertifications

Project Management

Certification

Knowledgehut

Leadership And Communications In ProjectsKnowledgehut

Microsoft Project 2007/2010-ae8d039bbd2a41318308f8d26b52ac8f.svg)

Knowledgehut

Financial Management For Project ManagersKnowledgehut

Fundamentals of Earned Value Management (EVM)Knowledgehut

Fundamentals of Portfolio ManagementKnowledgehut

Fundamentals of Program Management-35c169da468a4cc481c6a8505a74826d.webp&w=128&q=75)

Knowledgehut

CAPM® CertificationsKnowledgehut

Microsoft® Project 2016Certifications & Trainings

-7f4b4f34e09d42bfa73b58f4a230cffa.webp&w=128&q=75)

Knowledgehut

PMP® CertificationKnowledgehut

PMI-RMP® CertificationKnowledgehut

PMP Renewal Learning PathKnowledgehut

Oracle Primavera P6 V18.8Knowledgehut

Microsoft® Project 2013Knowledgehut

PfMP® Certification CourseKnowledgehut

Project Planning and MonitoringPrince2 Certifications

Knowledgehut

PRINCE2® FoundationKnowledgehut

PRINCE2® PractitionerKnowledgehut

PRINCE2 Agile Foundation and PractitionerKnowledgehut

PRINCE2 Agile® Foundation CertificationKnowledgehut

PRINCE2 Agile® Practitioner CertificationManagement Certifications

Knowledgehut

Project Management Masters Certification ProgramKnowledgehut

Change ManagementKnowledgehut

Project Management TechniquesKnowledgehut

Product Management Certification ProgramKnowledgehut

Project Risk Management- Study abroad

- Offline centres

- uGSOT - B.Tech

More

Economics Courses Online

Economics Courses Online help you understand how markets, governments, and businesses make decisions. Learn microeconomics, macroeconomics, policy analysis, and data interpretation. Build analytical skills to evaluate economic trends, solve real-world problems, and make informed financial and policy decisions.

20(1)-70997669bd1a4ba2b565901e0eae2fa5%20(1)-de9c82be352d44bcb6a48fecf60b4465.jpeg&w=3840&q=75)

Economics Masterclass Course Overview

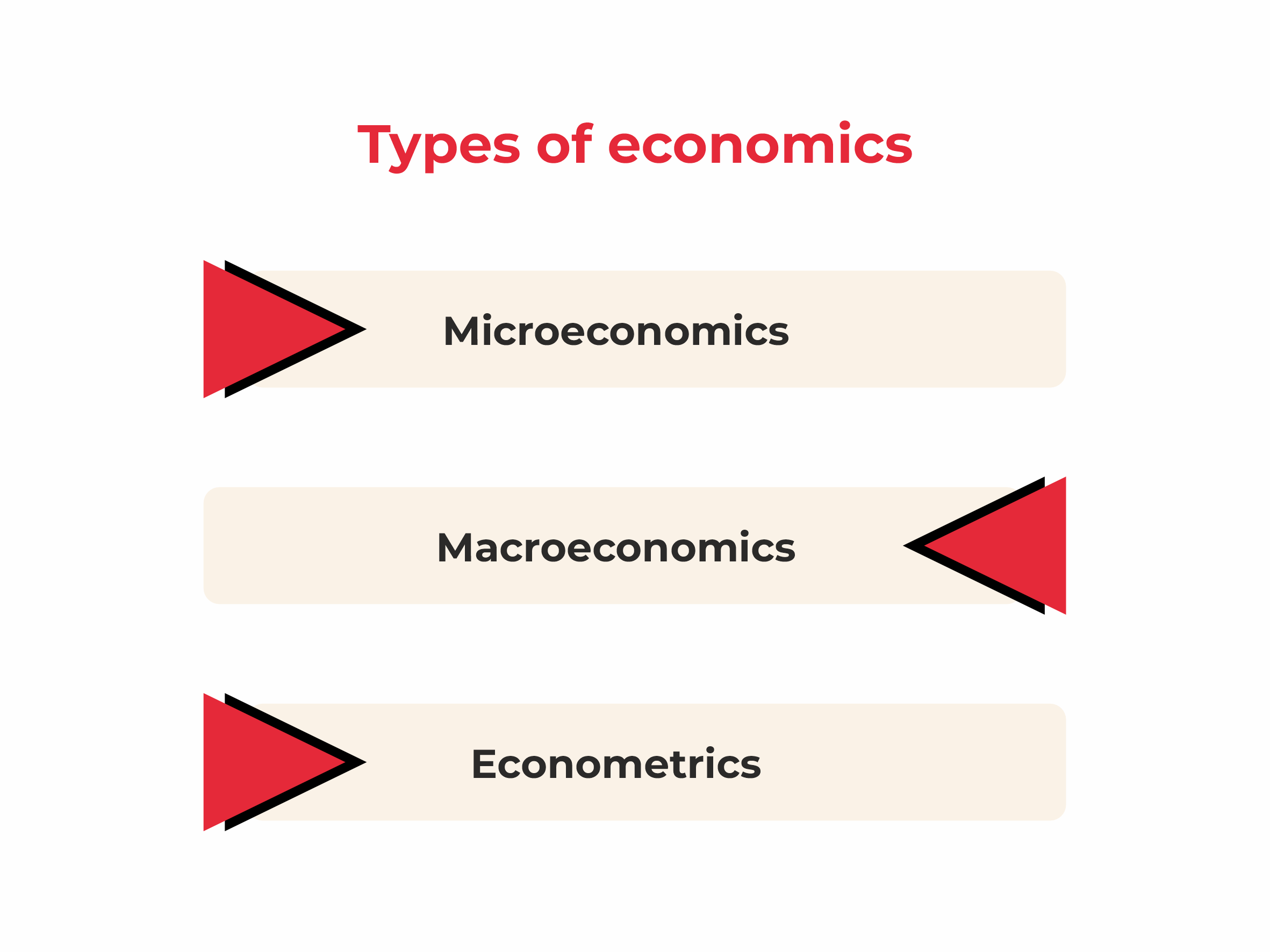

The subject area of economics analyses the behaviour and interactions of people while allocating scarce resources. It ensures the responsible and optimum utilisation of limited resources to maintain an ideal balance in the economy. It keeps a close check on the functions of the entire economy as well.

To properly manage every sector of the economy, there are two subsections of economics, Microeconomics and Macroeconomics. Besides these, other broad distinctions of economics are positive economics (what is), normative economics (what ought to be), economic theory and applied economics, rational economics, and behavioural economics.

The study of economics can be applied in several sectors of the economy like business, health care, finance, engineering, government, and even households.

Economics Course Instructors

Learn From The Best

Learn from industry leaders in our economics courses, offering real-world insights and expertise. Be the best by learning from the best in the industry.

12

Instructors

Success Stories

What Our Learners Have To Say

Learner Support and Services

How Will upGrad Supports You

upGrad Elevate: Virtual hiring drive giving you the opportunity to interview with upGrad's 300+ hiring partners

Job Opportunities Portal: Gain exclusive access to upGrad's Job Opportunities portal which has 100+ openings from upGrad's hiring partners at any given time

FAQs on Economics Masterclass Courses

1. What is the use of economics?

Economics is an imperative part of our life which extends across all aspects. Be it the optimum allocation of our resources or to generate maximum profit from a business, the knowledge of economics is essential

2. What are the key skills that students attain from economics courses?

Once a student learns economics, they attain quality skills that can benefit them to upscale their career. These skills include analytical and problem-solving skills, understanding the workings of the market, trends of the economy at large, and several other skills as well. All this adds up and helps the student be a professional with high demand.

3. Why is an Economics Specialist important in any Business?

It is essential to have an Economics Specialist in a growing Business to study the financial, market-related, organisational, and environmental issues individuals and organisations face. The economics specialists also focus on the production, distribution, and consumption chain.

4. What skills should I have to become an Economics Specialist?

There are a few skills that a person requires to become an Economics Specialist and to perform his task properly. Here are some of those skills;

- Mathematical Aptitude

- Better Understanding of Complex Systems

- Curious to learn more

- Knowledge of Social Sciences

- Comfortable with Uncertainty

- Independent Thinker

- Communication Skills

5. What are the key concepts in economics?

Some of the key concepts of economics are listed below;

- Scarcity

- Supply & Demand

- Incentives

- Costs & Benefits

- Inflation

- Investments

- Production, Distribution, and Consumption

6. Are students required to have economics and mathematics in class 11th or 12th to opt for economics courses?

No, there’s no compulsion as such to have economics or mathematics in previous classes. You can avail the online economics courses anytime as per your preference.

7. What kind of job positions are available after completing economics courses?

There are various job positions available after completing Economics Courses;

- Professional Economist

- Data Analyst

- Equity Analyst

- Data Scientist

- Research Associate

- Behaviour Analyst

- Product Development Scientist

- Economic Researcher

- Cost Accountant

8. What is the general duration for economics courses?

The typical duration to complete a graduation course in economics requires 3 years, and a Master’s course needs 2 years to finish.

9. How do businesses perceive the economics certification?

A person with an economics certification is respected in the professional field by the higher authorities because of their set of skills related to economics.

10. What is Econometrics?

It uses statistical and mathematical methods to develop economic theories and future trends by analysing and studying the historical data.

11. Why is it beneficial to take economics courses?

The field of economics is one of the progressing fields and has worldwide demand for its professionals. Once you acquire quality knowledge of economics, there are huge chances of you getting success in your career.

12. Which are the highest paying industries for Economics Specialists in India?

These are some of the professions of a particular industry that pays highly to economics specialists.

- Education

- Construction

- Travel

- Health Care

- Information and Technology

- Energy

- Banking

13. What is the highest pay for an Economics Specialist in India?

In India, the highest pay for an Economics Specialist is around Rs. 1,18,452 per month.

14. What are the highest paying jobs in economics in India?

- Market Research Analyst

- Credit Analyst

- Statistician

- Management Analyst

- Operation Research Analyst

15. What can an Economics Specialist do to increase their Salary?

To increase or promote yourself in your career and get a salary hike as an economics specialist, you must level up and include more of your skills. Moreover, an MBA or a master’s degree in this field can help you level up.

upGrad Learner Support

Talk to our experts. We are available 7 days a week, 10 AM to 7 PM

Indian Nationals

Foreign Nationals

Disclaimer

The above statistics depend on various factors and individual results may vary. Past performance is no guarantee of future results.

The student assumes full responsibility for all expenses associated with visas, travel, & related costs. upGrad does not .