All courses

Agentic AI

Agentic AI

IIIT Bangalore

Executive Programme in Generative AI for LeadersArtificial Intelligence

Degree / Exec. PG

IIIT Bangalore

Executive Diploma in Machine Learning and AI

OPJ Global University

Master’s Degree in Artificial Intelligence and Data Science

Liverpool John Moores University

Master of Science in Machine Learning & AI

Golden Gate University

DBA in Emerging Technologies with Concentration in Generative AIExecutive Certificate

IIITB & IIM, Udaipur

Chief Technology Officer & AI Leadership ProgrammeIIIT Bangalore

Executive Programme in Generative AI for Leaders

upGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftupGrad | Microsoft

Gen AI Mastery Certificate for Data AnalysisupGrad | Microsoft

Gen AI Mastery Certificate for Software DevelopmentupGrad | Microsoft

Gen AI Mastery Certificate for Managerial ExcellenceOffline Bootcamps

upGrad

Data Science and AI-MLDoctorate

For All Domains

IIITB & IIM, Udaipur

Chief Technology Officer & AI Leadership Programme

Swiss School of Business and Management

Global Doctor of Business Administration from SSBM

Edgewood University

Doctorate in Business Administration by Edgewood UniversityGolden Gate University

Doctor of Business Administration From Golden Gate University

Rushford Business School

Doctor of Business Administration from Rushford Business School, SwitzerlandGolden Gate University

Master + Doctor of Business Administration (MBA+DBA)-d9bdeff6165f4eb1ba2adcebde78e961.svg)

University of Waterloo

Chief Technology and AI Officer ProgramLeadership / AI

Golden Gate University

DBA in Emerging Technologies with Concentration in Generative AIMachine Learning

Machine Learning

Data Science

Degree / Exec. PG

O.P Jindal Global University

Master’s Degree in Artificial Intelligence and Data ScienceIIIT Bangalore

Executive Diploma in Data Science & AILiverpool John Moores University

Master of Science in Data ScienceExecutive Certificate

upGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftupGrad | Microsoft

Gen AI Mastery Certificate for Data AnalysisupGrad | Microsoft

Gen AI Mastery Certificate for Software DevelopmentupGrad | Microsoft

Gen AI Mastery Certificate for Managerial ExcellenceupGrad | Microsoft

Gen AI Mastery Certificate for Content CreationOffline Bootcamps

upGrad

Data Science and AI-MLupGrad

Data AnalyticsMBA

Masters

Paris School of Business

Master of Science in Business Management and TechnologyO.P.Jindal Global University

MBA (with Career Acceleration Program by upGrad)Edgewood University

MBA from Edgewood UniversityO.P.Jindal Global University

MBA from O.P.Jindal Global UniversityGolden Gate University

Master + Doctor of Business Administration (MBA+DBA)Executive Certificate

IMT, Ghaziabad

Advanced General Management ProgramMarketing

Executive Certificate

Offline Bootcamps

upGrad

Digital MarketingManagement

Degree

O.P Jindal Global University

MSc in International Accounting & Finance (ACCA integrated)Paris School of Business

Master of Science in Business Management and Technology

Golden Gate University

Master of Arts in Industrial-Organizational PsychologyExecutive Certificate

IIIT-B & IIM, Udaipur

Chief Technology Officer & AI Leadership Programme

IIM Kozhikode

Human Resource Analytics Course from IIM-KupGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftEducation

Education

Northeastern University

Master of Education (M.Ed.) from Northeastern UniversityEdgewood University

Doctor of Education (Ed.D.)Edgewood University

Master of Education (M.Ed.) from Edgewood UniversityCertifications

Project Management

Certification

Knowledgehut

Leadership And Communications In ProjectsKnowledgehut

Microsoft Project 2007/2010-ae8d039bbd2a41318308f8d26b52ac8f.svg)

Knowledgehut

Financial Management For Project ManagersKnowledgehut

Fundamentals of Earned Value Management (EVM)Knowledgehut

Fundamentals of Portfolio ManagementKnowledgehut

Fundamentals of Program Management-35c169da468a4cc481c6a8505a74826d.webp&w=128&q=75)

Knowledgehut

CAPM® CertificationsKnowledgehut

Microsoft® Project 2016Certifications & Trainings

-7f4b4f34e09d42bfa73b58f4a230cffa.webp&w=128&q=75)

Knowledgehut

PMP® CertificationKnowledgehut

PMI-RMP® CertificationKnowledgehut

PMP Renewal Learning PathKnowledgehut

Oracle Primavera P6 V18.8Knowledgehut

Microsoft® Project 2013Knowledgehut

PfMP® Certification CourseKnowledgehut

Project Planning and MonitoringPrince2 Certifications

Knowledgehut

PRINCE2® FoundationKnowledgehut

PRINCE2® PractitionerKnowledgehut

PRINCE2 Agile Foundation and PractitionerKnowledgehut

PRINCE2 Agile® Foundation CertificationKnowledgehut

PRINCE2 Agile® Practitioner CertificationManagement Certifications

Knowledgehut

Project Management Masters Certification ProgramKnowledgehut

Change ManagementKnowledgehut

Project Management TechniquesKnowledgehut

Product Management Certification ProgramKnowledgehut

Project Risk Management- Study abroad

- Offline centres

- uGSOT - B.Tech

More

FinTech Courses Online

Fintech Courses help you understand how technology is reshaping the world of finance. You’ll explore blockchain, AI, digital payments, and cybersecurity while gaining practical skills to work in banking, insurance, fintech startups, and tech-driven financial services.

20(1)-70997669bd1a4ba2b565901e0eae2fa5%20(1)-de9c82be352d44bcb6a48fecf60b4465.jpeg&w=3840&q=75)

FinTech Courses Online

The bitcoins you recently bought on Coinbase? FinTech. The online banking services you access via your smartphone? It’s FinTech in action. The PayPal payment you made for the new laptop you ordered online? Again, FinTech. The robo-advisors you turn to for financial planning advice? That’s FinTech too.

FinTech deploys easy-to-use technology to make financial services simpler and accessible to everyone. It removes the reliance on traditional banking systems and the need to set foot in brick-and-mortar financial institutions. From mobile banking and online payment platforms allowing users to make instant financial transactions to crypto and stock trading, there is virtually nothing FinTech cannot do.

FinTech empowers both businesses and consumers to take charge of their finances. It enhances financial literacy, breaking down silos and improving financial outcomes with the help of advanced technology. Although FinTech has been around for decades, it is only in the last few years that FinTech companies have transformed how people engage with financial services.

Let’s dive deep into FinTech and understand what it means.

FinTech Courses Instructors

Learn From The Best

Learn from industry leaders in FinTech courses and gain real-world insights to master digital finance, innovation, and emerging financial technologies.

12

Instructors

Success Stories

What Our Learners Have To Say

Learner Support and Services

How Will upGrad Supports You

upGrad Elevate: Virtual hiring drive giving you the opportunity to interview with upGrad's 300+ hiring partners

Job Opportunities Portal: Gain exclusive access to upGrad's Job Opportunities portal which has 100+ openings from upGrad's hiring partners at any given time

FAQs on FinTech Courses

1. What is FinTech?

FinTech combines the words “Financial” and “Technology.” It refers to any financial service that uses technology to design and deliver financial products and services such as lending, borrowing, mobile payments, viewing account balances and more.

2. Is PayPal a FinTech?

Yes, PayPal is a FinTech platform that offers online financial services such as banking and digital payments through mobile devices such as smartphones and tablets.

3. What is blockchain in FinTech?

Blockchain is a decentralised, distributed public ledger or database shared across a peer-to-peer computer network. A cryptocurrency is a digital currency based on blockchain technology secured through encryption.

4. What are the challenges faced by FinTech?

The major challenges faced by the FinTech industry include data security risks, regulatory compliance, lack of technical expertise and the need to provide a seamless user experience.

5. What are the types of FinTech?

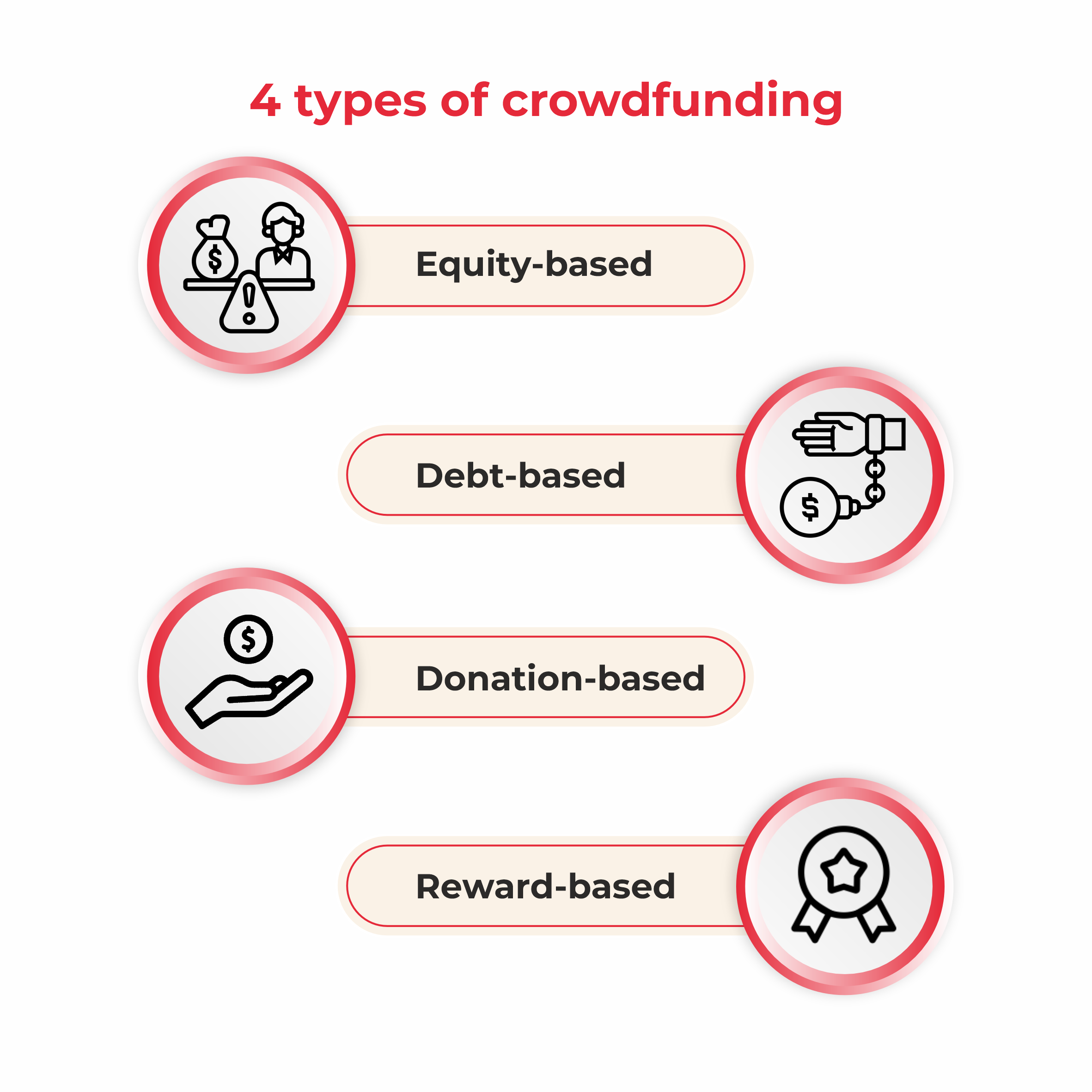

FinTech companies include insurance, mobile payments, international money transfers, crowdfunding platforms, stock trading apps, robo-advisors, cryptocurrency exchanges, equity financing and personal finance management apps.

6. What are the four categories of FinTech?

Four key segments in the FinTech industry include digital lending, payments, insurance and healthcare tech, and security technology.

7. What technology is used in FinTech?

Technologies in FinTech include machine learning, artificial intelligence, blockchain, robotic process automation (RPA), the internet of things (IoT) and others.

8. What are the benefits of FinTech?

Some of the key benefits of FinTech include faster, secure and more convenient financial transactions, more accessible funding, enhanced efficiency, greater customer retention, streamlined financial operations and better risk management.

9. How does FinTech affect the economy?

FinTech encourages the growth of a country's digital economy by promoting technological innovation. It improves the financial landscape of a country which directly impacts the economy.

10. Who uses FinTech?

Both consumers and businesses (B2B and B2C) use FinTech. You use FinTech every time you make an online payment via PayPal or Google Pay. Likewise, online banking apps available on Google Play or the App store are examples of FinTech.

11. Is Bitcoin a FinTech?

Bitcoin is a type of cryptocurrency or digital money. Cryptocurrencies, in turn, are a type of FinTech innovation.

12. How do banks use FinTech?

Applications of FinTech in the banking sector include biometric ATMs, smart chip ATM cards, mobile banking apps, AI-enabled customer service chatbots and e-wallets.

13. What is a FinTech product?

Mobile banking, online payment apps, robo-advisors, crowdfunding platforms, insurance technology, cryptocurrency exchanges, stock trading apps and personal finance management apps are examples of FinTech products.

14. What jobs are in FinTech?

Some prominent job roles in the FinTech industry include Specialists, cybersecurity professionals, Blockchain Developers, Quantitative Analysts, Data Scientists, Artificial Intelligence Experts, App Developers and Financial Analysts.

15. How do I learn FinTech?

You can enrol in any online FinTech certification course to start your learning journey. These online courses are flexible, convenient and relatively less expensive than traditional offline programs.

upGrad Learner Support

Talk to our experts. We are available 7 days a week, 10 AM to 7 PM

Indian Nationals

Foreign Nationals

Disclaimer

The above statistics depend on various factors and individual results may vary. Past performance is no guarantee of future results.

The student assumes full responsibility for all expenses associated with visas, travel, & related costs. upGrad does not .