All courses

Agentic AI

Agentic AI

Artificial Intelligence

Degree / Exec. PG

IIIT Bangalore

Executive Diploma in Machine Learning and AI

OPJ Global University

Master’s Degree in Artificial Intelligence and Data Science

Liverpool John Moores University

Master of Science in Machine Learning & AI

Golden Gate University

DBA in Emerging Technologies with Concentration in Generative AIExecutive Certificate

IIITB & IIM, Udaipur

Chief Technology Officer & AI Leadership Programme

IIIT-B & IIM, Udaipur

Chief Data and AI Officer Programme

IIIT Bangalore

Executive Programme in Generative AI for Leaders

upGrad | Microsoft

Gen AI Mastery Certificate for Software DevelopmentOffline Bootcamps

upGrad

Data Science and AI-MLDoctorate

For All Domains

IIITB & IIM, Udaipur

Chief Technology Officer & AI Leadership Programme

Swiss School of Business and Management

Global Doctor of Business Administration from SSBM

Edgewood University

Doctorate in Business Administration by Edgewood UniversityGolden Gate University

Doctor of Business Administration From Golden Gate University

Rushford Business School

Doctor of Business Administration from Rushford Business School, Switzerland-d9bdeff6165f4eb1ba2adcebde78e961.svg)

University of Waterloo

Chief Technology and AI Officer ProgramLeadership / AI

Golden Gate University

DBA in Emerging Technologies with a concentration in Generative and Agentic AIMachine Learning

Machine Learning

Data Science

Degree / Exec. PG

O.P Jindal Global University

Master’s Degree in Artificial Intelligence and Data ScienceIIIT Bangalore

Executive Diploma in Data Science & AILiverpool John Moores University

Master of Science in Data ScienceExecutive Certificate

upGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftIIIT-B & IIM, Udaipur

Chief Data and AI Officer ProgrammeupGrad | Microsoft

Gen AI Mastery Certificate for Data AnalysisupGrad | Microsoft

Gen AI Mastery Certificate for Software DevelopmentupGrad | Microsoft

Gen AI Mastery Certificate for Managerial ExcellenceupGrad | Microsoft

Gen AI Mastery Certificate for Content CreationOffline Bootcamps

upGrad

Data Science and AI-MLMBA

Masters

Liverpool John Moores University

Master of Business Administration from Liverpool John Moores University (LJMU) with IIM Udaipur CertificationO.P.Jindal Global University

MBA (with Career Acceleration Program by upGrad)Edgewood University

MBA from Edgewood UniversityO.P.Jindal Global University

MBA from O.P.Jindal Global UniversityExecutive Certificate

IMT, Ghaziabad

Advanced General Management ProgramMarketing

Executive Certificate

upGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftupGrad | Microsoft

Gen AI Mastery Certificate for Content CreationOffline Bootcamps

upGrad

Digital MarketingManagement

Degree

O.P Jindal Global University

MSc in International Accounting & Finance (ACCA integrated)

Golden Gate University

Master of Arts in Industrial-Organizational PsychologyExecutive Certificate

IIIT-B & IIM, Udaipur

Chief Technology Officer & AI Leadership ProgrammeIIIT-B & IIM, Udaipur

Chief Data and AI Officer Programme

IIM Kozhikode

Human Resource Analytics Course from IIM-KupGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftEducation

Education

Northeastern University

Master of Education (M.Ed.) from Northeastern UniversityEdgewood University

Doctor of Education (Ed.D.)Edgewood University

Master of Education (M.Ed.) from Edgewood UniversityCertifications

Project Management

Certification

Knowledgehut

Leadership And Communications In ProjectsKnowledgehut

Microsoft Project 2007/2010-ae8d039bbd2a41318308f8d26b52ac8f.svg)

Knowledgehut

Financial Management For Project ManagersKnowledgehut

Fundamentals of Earned Value Management (EVM)Knowledgehut

Fundamentals of Portfolio ManagementKnowledgehut

Fundamentals of Program Management-35c169da468a4cc481c6a8505a74826d.webp&w=128&q=75)

Knowledgehut

CAPM® CertificationsKnowledgehut

Microsoft® Project 2016Certifications & Trainings

-7f4b4f34e09d42bfa73b58f4a230cffa.webp&w=128&q=75)

Knowledgehut

PMP® CertificationKnowledgehut

PMI-RMP® CertificationKnowledgehut

PMP Renewal Learning PathKnowledgehut

Oracle Primavera P6 V18.8Knowledgehut

Microsoft® Project 2013Knowledgehut

PfMP® Certification CourseKnowledgehut

Project Planning and MonitoringPrince2 Certifications

Knowledgehut

PRINCE2® FoundationKnowledgehut

PRINCE2® PractitionerKnowledgehut

PRINCE2 Agile Foundation and PractitionerKnowledgehut

PRINCE2 Agile® Foundation CertificationKnowledgehut

PRINCE2 Agile® Practitioner CertificationManagement Certifications

Knowledgehut

Project Management Masters Certification ProgramKnowledgehut

Change ManagementKnowledgehut

Project Management TechniquesKnowledgehut

Product Management Certification ProgramKnowledgehut

Project Risk Management- Study abroad

- Offline centres

- uGSOT - B.Tech

More

%20(2)-db0b6f38da9c485faf76e366793c9b9e.webp&w=128&q=75)

Microeconomics Courses Online

Microeconomics Courses help you understand how people, businesses, and governments make choices when resources are limited. You’ll learn how prices are set, how markets work, and how competition or monopoly affects decisions, giving you practical insights into everyday economic behavior.

20(1)-70997669bd1a4ba2b565901e0eae2fa5%20(1)-de9c82be352d44bcb6a48fecf60b4465.jpeg&w=3840&q=75)

Microeconomics Course Overview

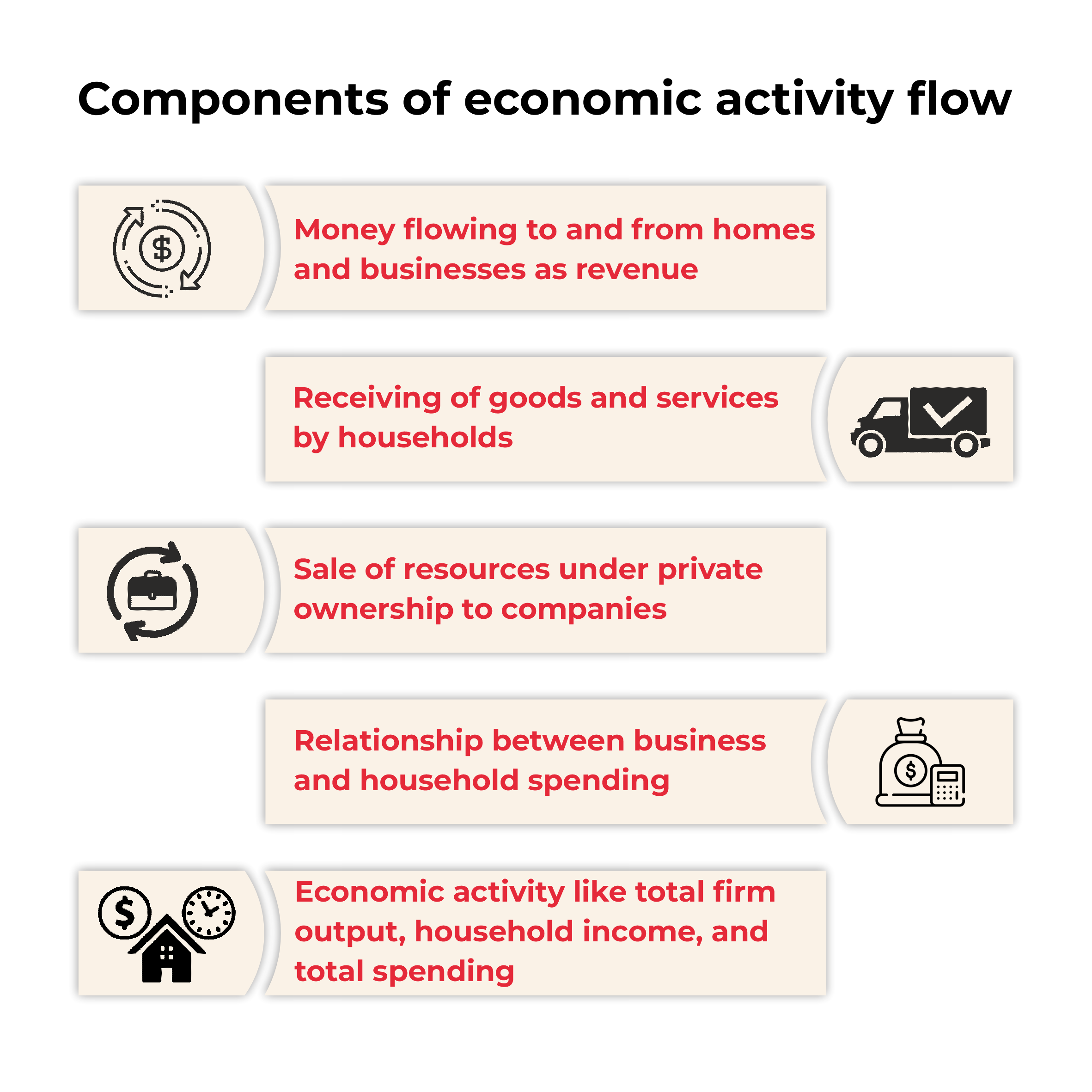

Microeconomics and Macroeconomics constitute the two nodal branches of economics. In Microeconomics, individuals are often categorised as belonging to microeconomic subgroups such as business owners, buyers and sellers. The study of microeconomics is basically an analysis of the tendencies that are supposed to originate when these individual actors make a decision. Changes with reference to incentives, resources and prices of production coupled with production methods are recorded.

Positive microeconomics discusses economic behaviour and what to expect when particular variables change. Positive microeconomics tends to provide insight into a company's sales, productivity and profit based on any recent changes in their manufacturing or marketing strategy.

These insights are then used to prescribe the course of action for these companies or governments to work effectively and undertake measures such that their profits remain intact and the demand chain is sated.

Microeconomics Course Instructors

Learn From The Best

Learn from industry leaders in our microeconomics courses, offering real-world insights and expertise. Be the best by learning from the best in the industry.

12

Instructors

Success Stories

What Our Learners Have To Say

Learner Support and Services

How Will upGrad Supports You

upGrad Elevate: Virtual hiring drive giving you the opportunity to interview with upGrad's 300+ hiring partners

Job Opportunities Portal: Gain exclusive access to upGrad's Job Opportunities portal which has 100+ openings from upGrad's hiring partners at any given time

FAQs on Microeconomics Courses

1. Which instances of microeconomics are there?

Because a product's price has gone up, demand in a certain market has decreased. Another illustration is a company expanding its resources to provide additional items.

2. Which three principles of microeconomics dominate?

The three key ideas are supply and demand, consumer behaviour, and income levels. The greatest research has been done on these ideas for tracking microeconomic data.

3. Simply put, what is microeconomics?

The acts and conduct of families and enterprises are the main topics of microeconomics. Microeconomics demonstrates the fundamental movement of resources, money, products, and services.

4. What subject areas does microeconomics cover?

Microeconomics addresses issues related to how families and companies interact. The primary subjects are supply and demand, equilibrium, competition, profit maximisation, and opportunity cost.

5. Is Opportunity Cost Real?

The financial accounts of a corporation do not immediately reflect opportunity costs. However, from an economic perspective, opportunity costs remain quite significant. Opportunity cost is a somewhat abstract idea, though, so many businesses, executives, and investors neglect to consider it while making daily decisions.

6. What four distinct client purchase behaviours are there?

There are four different forms of consumer behaviour: complicated buying behaviour, dissonance reduction, variety seeking, and habitual buying behaviour. The sort of product a customer requires, their degree of engagement, and the variations across companies all influence the many forms of consumer behaviour.

7. What kind of customer behaviour would that be?

Take choosing a city getaway for two as an illustration of consumer behaviour. It could need substantial decision-making for someone just starting to date, but it might just require minimal decision-making for a couple dating for at least five years.

Making a reservation at a restaurant is another instance of customer behaviour. Scheduling a reservation for a night out with friends just takes a short amount of time; however, making one for an anniversary or a marriage proposal takes more thought.

8. What distinguishes perfect from the imperfect competition?

In a market with perfect competition, all providers engage in fair competition. Contrarily, competition is vulnerable to imbalances in imperfect markets where businesses do not compete on an even playing field.

upGrad Learner Support

Talk to our experts. We are available 7 days a week, 10 AM to 7 PM

Indian Nationals

Foreign Nationals